What Is Tap-to-Pay and How Does It Work? A Complete Guide

None of this rules out tap-to-pay in Nigeria. It simply means the country is earlier on the adoption curve than South Africa or Morocco, with infrastructure catching up piece by piece.

Ten years ago, paying for a coffee meant handing over a card and waiting for a machine to accept it, or counting out change. Today, in shops from Cape Town to Casablanca, that whole exchange has shrunk to about a second: a phone or card held near a small reader, a short beep, and the receipt is printing before the wallet is put away. That single motion, generally known as tap-to-pay, is fast becoming the default way people pay for everyday things across much of the world, and Africa is no exception.

What is Tap-to-Pay?

Tap-to-pay is a way of paying for something by holding a card, phone, or wearable device near a payment terminal, rather than inserting a card or typing in a PIN. It runs on a short-range wireless technology called Near-Field Communication, or NFC. NFC itself belongs to a wider family of technology called radio-frequency identification, the same basic idea that has been used for decades to scan groceries and track luggage. What sets NFC apart is how little range it needs to work; in practice, a card or phone has to come within a few centimetres of the reader before anything happens, which is part of why the payment feels almost instant. This is also why tap-to-pay is often called a contactless payment. There is no chip to insert, no swipe, and no real contact with the machine at all.

How Does Tap-to-Pay Actually Work?

When a card or phone is held near an NFC-enabled terminal, the two exchange encrypted information over that short radio link. Rather than sending the actual card number, most tap-to-pay transactions today rely on a process called tokenisation. The real card number is replaced with a substitute number, or token, stored on the phone or card, which means nothing to anyone who happens to intercept it.

Alongside the token, a fresh code called a cryptogram is generated for every single transaction, so even if someone copied the data from one tap, it could not be reused for another. Within roughly one to two seconds, the terminal confirms the payment, and the transaction is done. Using a tap-to-pay card needs no setup beyond checking for the contactless symbol, a small set of curved radio-wave lines (like the Wi-Fi symbol) printed on the card, which shows it is NFC-enabled.

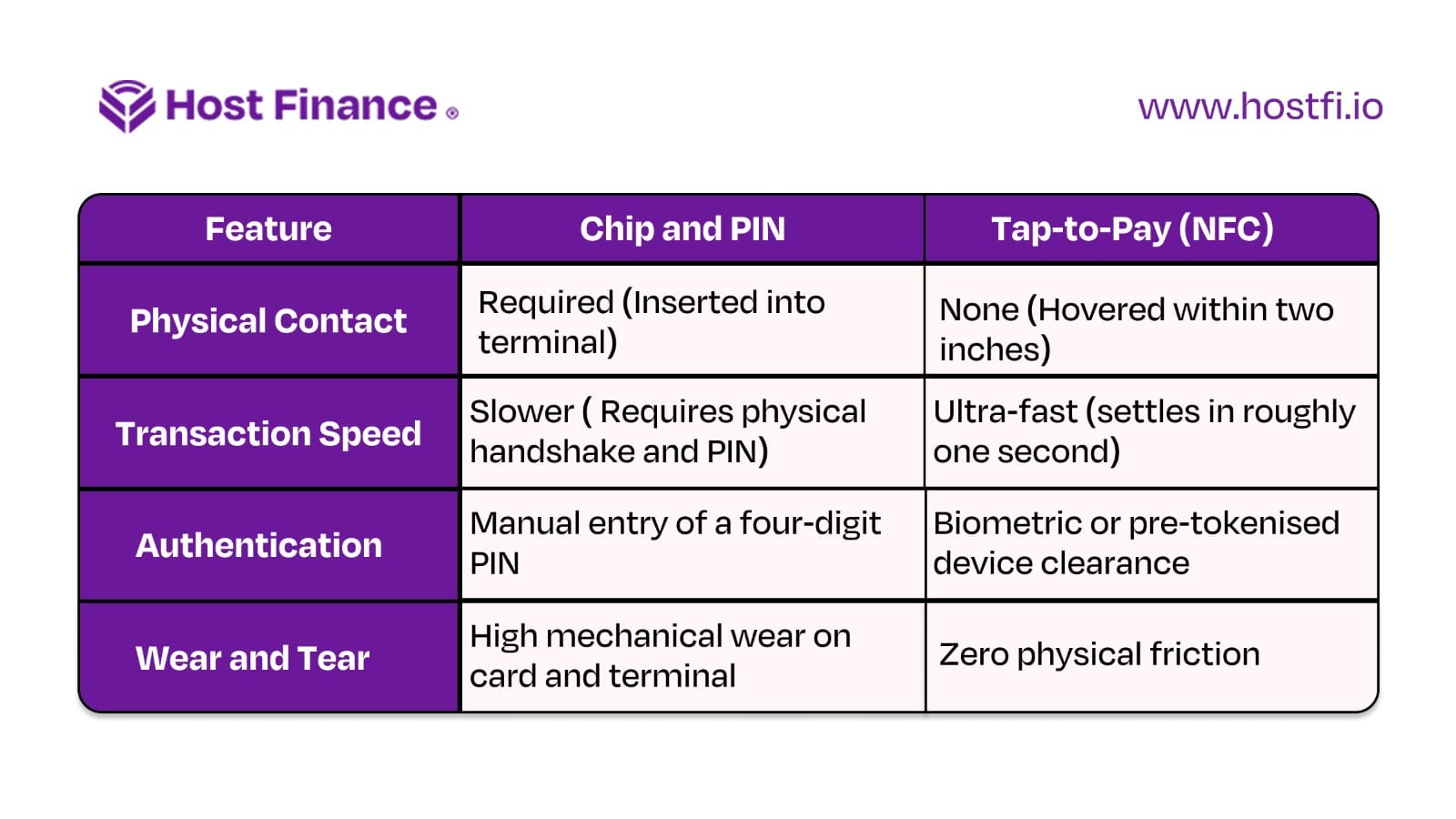

How Does Tap-to-Pay Compare with Chip-and-PIN?

Chip-and-PIN cards are generally considered safer than the old magnetic stripe, but the chip has to communicate with the terminal for several seconds while it checks the transaction, which is why those payments can feel slow, especially with a queue building behind you. Tap-to-pay skips that back-and-forth for smaller amounts and settles the payment almost immediately. For anything above the amount a bank or regulator sets as safe to approve without extra checks, most systems will still ask for a PIN or another form of verification, so the convenience does not come at the cost of security on larger purchases.

Where is Tap-to-Pay Catching on Across Africa?

Adoption varies sharply by country. South Africa is generally seen as the continent's most advanced contactless market. During 2020, as shoppers looked for ways to avoid touching shared payment terminals, the number of contactless transactions in South African grocery and pharmacy stores grew 13 times over compared with the year before, and a Mastercard consumer study found that 75% of South African shoppers had started using contactless payments. That habit has largely stuck.

In Morocco, more than 55% of card transactions are now completed by tapping rather than inserting, helped along by wider issuance of NFC-enabled cards from local banks. Kenya's contactless growth has taken a different shape, layering NFC card and phone payments on top of an already dominant mobile money network built around M-Pesa. Ghana's major banks have also begun issuing contactless cards, though acceptance among smaller merchants is still catching up.

Even with this momentum, cash has not disappeared from the picture. In Nigeria, for instance, cash still accounted for 40% of point-of-sale transactions in 2024, down from 91% in 2019, which is proof enough that the shift toward digital and contactless payments is well underway but not finished, even in a market moving quickly.

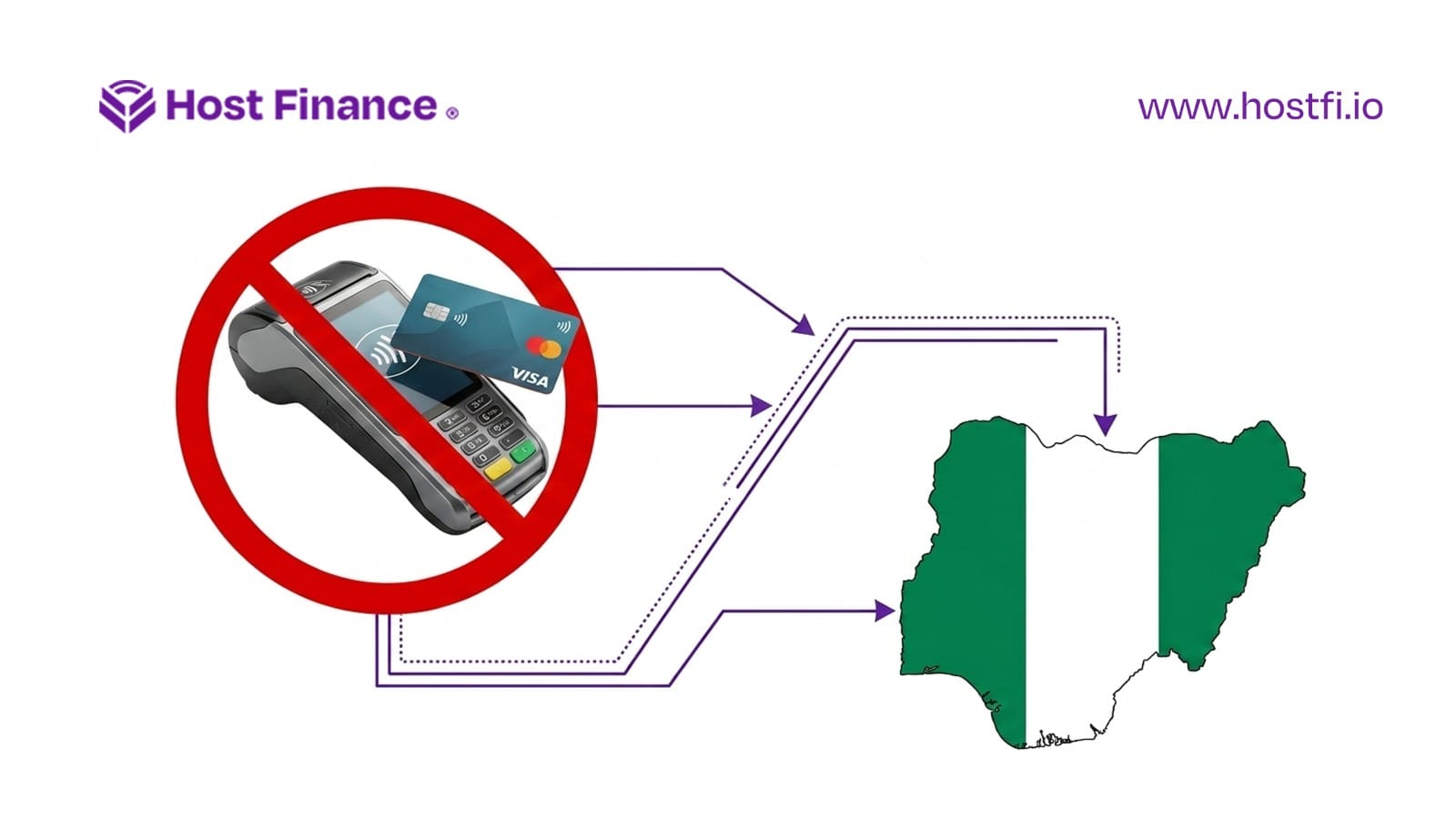

Why Isn't Tap-to-Pay Fully Available in Nigeria Yet?

Nigeria's answer is more nuanced than a simple yes or no. Contactless cards already exist here. AfriGO, the domestic card scheme, partnered with Moniepoint to issue 5 million contactless cards, and Verve and other issuers have added NFC to new cards as well. What is missing is the fuller mobile wallet experience that many people picture when they hear “tap-to-pay”. As of 2026, Apple Pay is still not officially available in Nigeria, despite the country having one of Africa's largest iPhone user bases.

Regulation plays a part too. The Central Bank of Nigeria's Guidelines on Contactless Payments, issued on June 27, 2023, set a single transaction limit of ₦15,000 and a daily cumulative limit of ₦50,000 for contactless payments made without a PIN or biometric check. Anything above that requires extra verification. Most Nigerian merchants also still use older point-of-sale hardware built for card insertion rather than tapping, and the runaway success of NIBSS Instant Payment, the bank transfer system most Nigerians already trust, has left merchants with less pressure to upgrade their terminals. None of this rules out tap-to-pay in Nigeria. It simply means the country is earlier on the adoption curve than South Africa or Morocco, with infrastructure catching up piece by piece.

Frequently asked questions

Is Tap-To-Pay Safe?

Generally, yes, more so than older payment methods. Tokenisation means the terminal never sees the real card number, and a fresh cryptogram is generated for every transaction, which makes stolen data very hard to reuse.

Does Tap-To-Pay Need Internet?

The tap itself works over a short-range radio signal and does not need a phone's data connection to complete. The payment terminal, however, usually needs a network connection to process and confirm the transaction with the bank.

What Is the Difference Between Tap-To-Pay and QR Code Payment?

Tap-to-pay uses NFC, with a card, phone, or wearable held near a reader. QR code payment works by scanning a printed or displayed code with a phone's camera. Both count as contactless in the sense that no card needs to be inserted, but the technology underneath is different.

Why Isn't Apple Pay in Nigeria Yet?

Apple has not given an official reason. The likely factors are the deep banking integrations Apple typically requires before launch, existing CBN regulation around digital payments, and the smaller number of NFC-ready payment terminals historically deployed by Nigerian merchants.

The Mechanism Behind the Tap

Tap-to-pay is no longer a novelty. It is quickly becoming the default way of paying in some of the world's biggest markets, and African adoption, while uneven, is heading the same way. For Nigerians earning or holding value in crypto, that shift matters in a practical sense.

Platforms like HostFi let users fund a virtual card directly from naira or crypto and tap to pay wherever contactless is accepted, including abroad. To see what that looks like in practice, our guide on How to Travel Cashless With Crypto walks through exactly how it works.